In last century, We have seen many changes in the global economy and the political landscape over the years. One of the most significant changes was the end of the Bretton Woods system and the delinking of the US dollar from gold.

The Bretton Woods system, established after World War II, fixed the value of the US dollar to gold at a rate of $35 per ounce. Other countries pegged their currencies to the US dollar, and the value of their currencies in relation to gold was determined by the fixed exchange rate. This system worked well in the early post-war years, but by the early 1960s, the US dollar was overvalued and the system was under increasing strain.

President Lyndon B. Johnson’s Great Society programs, which aimed to reduce poverty and racial inequality in the United States, required significant domestic spending. At the same time, the US was increasing its military involvement in Vietnam, resulting in a sharp increase in military spending. These factors worsened the overvaluation of the US dollar, as they led to a growing trade deficit and an outflow of gold reserves from the US. As the 1960s progressed, more and more countries sought to exchange their dollar holdings for gold, leading to a steady outflow of assets from the US.

The United States’ balance of payments deficit was not only increasing but also accelerating in 60s. However, the Fed was able to finance it by luring foreign central banks and private banks to purchase US Treasury bonds. These Treasury bills were the easiest way to get hold of dollars for private banks and foreign central banks to finance their companies’ international commercial activities.

In France, The Bretton Woods system was called privilège exorbitant du dollar (Dollar’s Exorbitant Privilege) as it resulted in an “asymmetric financial system” where non-US citizens see themselves supporting American living standards and subsidizing American multinationals.

In simple terms, the US government could print more money to finance their expenditures and debt, while other countries had to back their currencies with actual goods. This created a situation where the US could benefit from the exorbitant privilege of being able to print money at a low cost while other countries were essentially forced to pay for it. This imbalance caused tension, and in 1965, French President Charles de Gaulle announced that France would begin exchanging its US dollar reserves for gold at the official exchange rate.

By 1968, the gold market was split into two: an official market reserved for international institutions, selling gold at a fixed price of $35 per ounce, and a free market for the private sector where gold was worth considerably more. This division made it evident that the dollar was losing its trustworthiness.

Frustrated with the situation, France and Germany decided to exchange their dollars for gold that was stored at the Fed, which resulted in the reduction of the US gold reserve. The French President Charles de Gaulle even took the bold step of chartering a French warship, the Colbert, to hasten the repatriation of the yellow metal, as disclosed later by Valery Giscard d’Estaing, his advisor at the time.

The fear that other countries might follow suit loomed large as the Fed’s gold reserve could cover only 20% of the dollar reserves held by foreign central banks. In 1971, the United Kingdom also warned of its intention to repatriate large amounts of its gold. The situation was alarming, and a significant shift was imperative.

The situation worsened with Germany’s withdrawal from the Bretton Woods agreement, triggering a wave of panic and currency crises. By June 1971, the US had lost $22 billion in assets. In July, Switzerland exchanged $50 million of its dollar holdings for gold, and one month later, it pulled the Swiss Franc from the Bretton Woods system. France also redeemed $191 million for gold in August, sending a destroyer to New York Harbor to collect the gold from the Federal Reserve and bring it back to France.

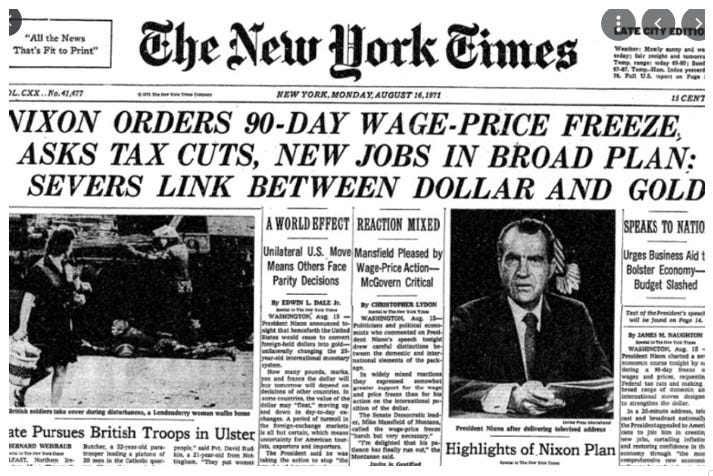

The US government faced a dilemma: it could either reduce its domestic spending and military commitments, or it could devalue the dollar against gold to restore balance to the international monetary system. In 1971, President Richard Nixon chose the latter option, announcing that the US would no longer exchange dollars for gold at a fixed rate. This move, known as the Nixon Shock, effectively ended the Bretton Woods system and marked the beginning of a new era of floating exchange rates.

After the end of the Bretton Woods system, the US dollar did not collapse because the United States remained the world’s largest economy and had a strong military presence around the world. The US dollar also remained the dominant currency for international trade and financial transactions, giving it a powerful advantage. Additionally, the US Federal Reserve and other central banks implemented policies to stabilize currency exchange rates and prevent a sudden collapse of the US dollar. These policies included managing interest rates, intervening in foreign exchange markets, and coordinating with other central banks. The US government also implemented fiscal policies to address balance of payments issues, such as reducing government spending and increasing exports.

EURO : The First Challenger to privilège exorbitant du dollar

In Mid 90s, Some bigwigs in the finance world were saying that the euro could give the dollar a run for its money. Even Alan Greenspan, the former boss of the US Federal Reserve, said not too long ago that it’s entirely possible that the euro might replace the dollar as the go-to reserve currency, or at least become a similarly important one. And get this —as far back as 1995, econometric analysis suggested that the euro could become the leading reserve currency, provided two conditions were fulfilled.

The first condition was that all remaining members of the EU, including the UK, would adopt the euro by 2020.

The second condition for the euro to replace the dollar as the major reserve currency was that the European Union would need to create a deep and liquid financial market.

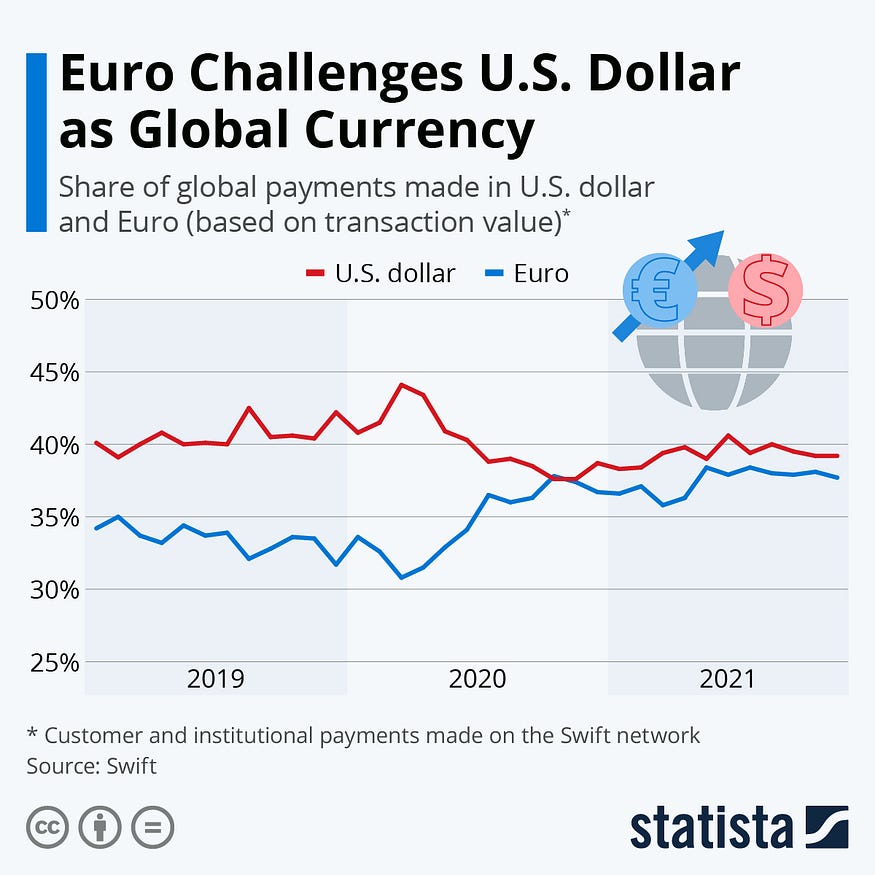

The euro has made significant strides as a currency, but it still hasn’t overtaken the US dollar as the world’s main reserve currency. The US dollar remains the go-to currency for international trade and finance, while the euro grapples with challenges such as the debt crisis in some European countries, Brexit and the absence of a cohesive fiscal policy across the EU. Nonetheless, there are still financial experts who hold on to the idea that the euro may eventually give the US dollar a run for its money in the global economy.

Yuan : A Rising Challenger to the mighty Dollar

So, there’s been a lot of buzz lately about the Chinese yuan giving the US dollar a run for its money. Apparently, lots of countries are getting antsy about how dependent they are on the dollar, especially with all the financial sanctions the US has been dishing out to places like Russia. The Covid-19 pandemic and the Ukraine war have shaken things up even more, with the dollar losing its top spot and the yuan making gains in the global foreign exchange reserves game.

And get this: even the International Monetary Fund is talking about it! Their report, the Composition of Official of Foreign Exchange Reserves (COFER), showed that while the global foreign exchange reserves went up to $12.85 trillion in Q3 of 2021, the US dollar’s share actually went down to 59.2%.

Now, I know what you’re thinking: the US dollar, British pound, Japanese yen, and European euro are still the big dogs, right? Well, yeah, they’re definitely still holding down the fort. But here’s the kicker: in 1999, those four currencies made up a whopping 98% of world foreign exchange reserves. Fast forward to 2021, and that number has dropped to 92%. The IMF report suggests that rather than picking up the slack, central banks of the world are starting to diversify their holdings for other currencies beyond the usual suspects. Things are definitely heating up in the currency world!

Another thing to note here is, share of central bank reserves.

The yuan has been gaining ground in this domain, with a 25% share of central bank reserves worldwide by the end of 2020, making it the largest component of non-traditional currencies in global reserves. This trend towards the yuan is a significant step towards “de-dollarization” and reducing dependence on the US dollar. In 2016, the yuan was the first emerging-market currency to be included in IMF Special Drawing Rights, previously a privilege of only the big four currencies. Russia has been increasingly settling its monetary transactions with yuan due to their growing trade and political relations. This has led to a surge in yuan’s share in Russia’s foreign exchange reserves, rising from 12.8% to 17.1% in January 2022, while the US dollar’s share plummeted from 21.1% to 10.9% over the same period.

The main challenge for mighty Dollar is, If more countries decide to trade using their own currencies, it could decrease the demand for the US dollar, potentially causing it to lose value.

In a recent move, China and Brazil have agreed to conduct their trade and financial transactions using their respective currencies. This means that they will no longer rely on the US dollar as an intermediary, and instead will directly exchange yuan for reais, and vice versa.

China made same agreement with Russia, Saudi Arabia, Iran, South Africa and many more. Japan and China already agreed in 2011 to dump the US dollar and trade with their respective currencies.

De-dollarization is not limited to China alone. Other countries are also taking steps to reduce their reliance on the US dollar in international trade and finance. India, for example, has also been moving towards de-dollarization in recent years. In 2019, the Reserve Bank of India (RBI) signed a currency swap agreement with the Bank of Japan, which allowed for the exchange of their respective currencies up to a limit of $75 billion. Moreover, India has been diversifying its foreign exchange reserves away from the US dollar and towards other currencies such as the euro, yen, and yuan. In 2020, the RBI increased its holdings of gold as a means of further diversification. India has also been encouraging the use of its own currency, the rupee, in cross-border trade with neighboring countries such as Nepal, Bhutan, Malaysia, Sri Lanka and Bangladesh. It has been promoting the use of the rupee as a settlement currency in trade with Iran, which has been subject to US sanctions.

But the Trillion Dollar Question is, whether it’s possible to topple the dollar from its throne?

The Answer is Yes but it’s not an easy task. You see, the US economy is the world’s largest and most stable, making the US dollar a reliable currency for international transactions. Furthermore, the US government and financial institutions are unlikely to give up the advantages of the US dollar without a fight. They have a vested interest in maintaining the US dollar’s dominance, and they will likely take steps to protect it.

The main threat to dollar is not coming from Euro, Yuan or Rupee but from the US itself.

Let me explain, Dollar’s Exorbitant Privilege is rooted in the economic strength of the United States and the trust that the international community has in its economic system. But the economic power of US is declining and trust in dollar is eroding and there are many reasons for this.

- The Mighty Dollar’s Weaponization:

The US has long used its position as the world’s leading reserve currency to exert its influence on other countries, by imposing sanctions, tariffs, or withholding access to the US financial system. SWIFT, an acronym of Society for Worldwide Interbank Financial Telecommunication, is often used as a tool to sanction countries. It has been used against Belarus, Iran and Russia. However, it has also caused resentment and resistance among other countries, who seek to reduce their dependence on the dollar and establish alternative payment system.

2. US debt :

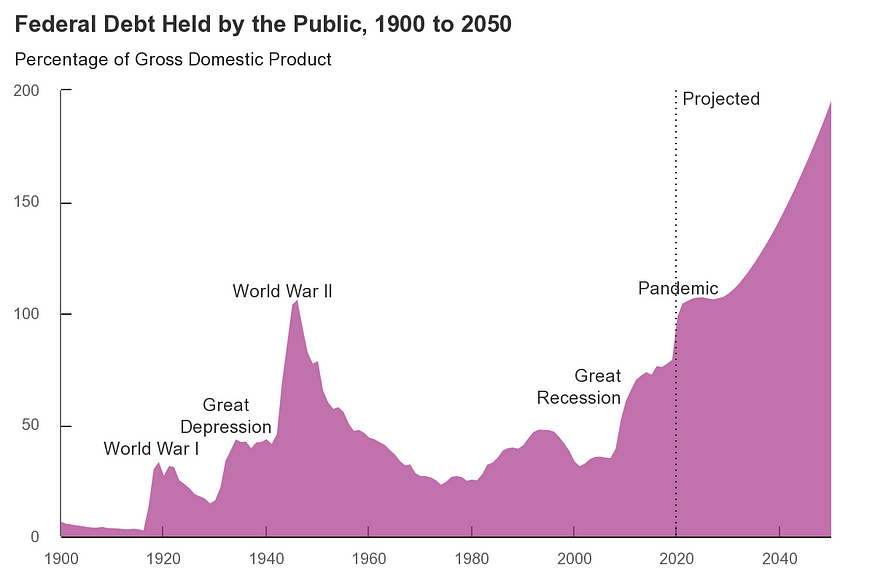

The U.S. national debt has been steadily rising for years, and as of 2023, Government debt accounted for 123.4 % of the country’s Nominal GDP i.e around 31 Trillion USD. This could potentially lead to the downfall of the dollar. As the government continues to spend more than it brings in through taxes, it must borrow money to make up the difference. This results in an ever-increasing debt that is unsustainable in the long run. As the debt grows, investors may lose confidence in the government’s ability to pay it back, leading to a decrease in demand for U.S. treasuries. This, in turn, would cause interest rates to rise, making it more expensive for the government to borrow money and increasing the cost of servicing the debt. If this were to continue, it could eventually lead to hyperinflation and a collapse of the dollar as a viable currency.

3. Oil geopolitics — PetroDollar at risk

In 2023, there are some changes that suggest the petrodollar may not be as strong as previously thought, and that the US may need to reassert its dominance. The most significant change occurred on March 29 when Saudi Arabia announced its plan to become a “dialogue partner” with the Shanghai Cooperation Organization, which is the world’s largest regional defense and political organization in terms of population and geographical scope. Moreover, at the World Economic Forum in Davos, the Finance Minister of Saudi Arabia, Mohammed Al-Jadaan, stated that “there are no issues discussing how we settle our trade arrangements, whether it’s in the US dollar, the euro, or the Saudi riyal.” Although Saudi Arabia has not abandoned the petrodollar, its actions indicate that it may be exploring other options. Since Saudi Arabia is the keystone of the petrodollar, if they start to trade oil in yuan, other OPEC members may follow suit, leading to a domino effect.

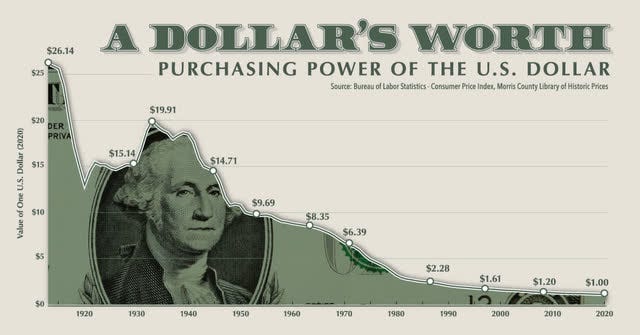

4. Decline of Purchasing Power of US Dollar and Inflation:

Inflation erodes the purchasing power of the currency, which makes imports more expensive and ultimately leads to a decrease in demand for the currency. As the demand for the dollar decreases, its value falls, which can further exacerbate inflation. If this trend continues, it could lead to a vicious cycle that ultimately results in a collapse of the dollar.

Furthermore, if the US government continues to borrow heavily and rely on the printing of more money to finance its operations, it could lead to hyperinflation and the complete devaluation of the dollar. This could cause people to lose faith in the currency, which would result in a massive sell-off and further depreciation of the dollar’s value

Conclusion:

So there you have it, folks! The collapse of the mighty dollar is not just a far-fetched idea anymore. With the current economic situation, the US government’s debt, and the growing trend of de-dollarization, the possibility of the dollar’s downfall is becoming more and more real. The decline in purchasing power and inflation are just some of the factors that can lead to the dollar’s collapse. It remains to be seen what the future holds for the dollar, but one thing is for sure, the world is changing, and so are the dynamics of global currencies.

Follow me :

https://medium.com/@trendingtribes

https://instagram.com/@trendingtribes

Comments

Post a Comment